Collateral-Free Business Loans in India: The Complete 2026 Guide

This guide explains collateral-free business loan for Indian startups and MSMEs — clearly and practically.

Most small businesses stall because they lack assets to pledge. The good news: India now has several genuine collateral-free funding routes.

In this guide, the team at Ashvya Services breaks down everything Indian founders and MSME owners need to know about collateral-free business loan — practically, and without the jargon.

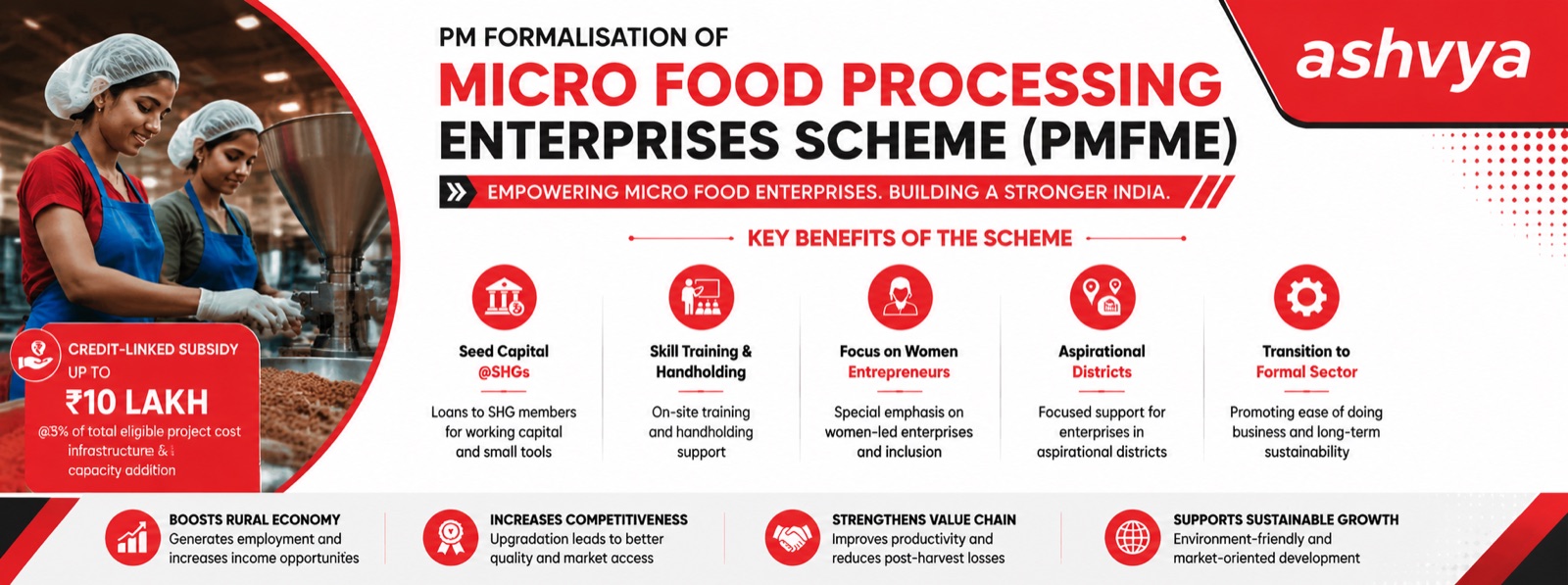

Understanding collateral-free business loan: What CGTMSE means for you

Under the CGTMSE scheme, lenders can offer credit without collateral because the government guarantees a large share of the loan.

- Credit up to ₹5 crore

- No third-party collateral or guarantee

- Available to most manufacturing and service MSMEs

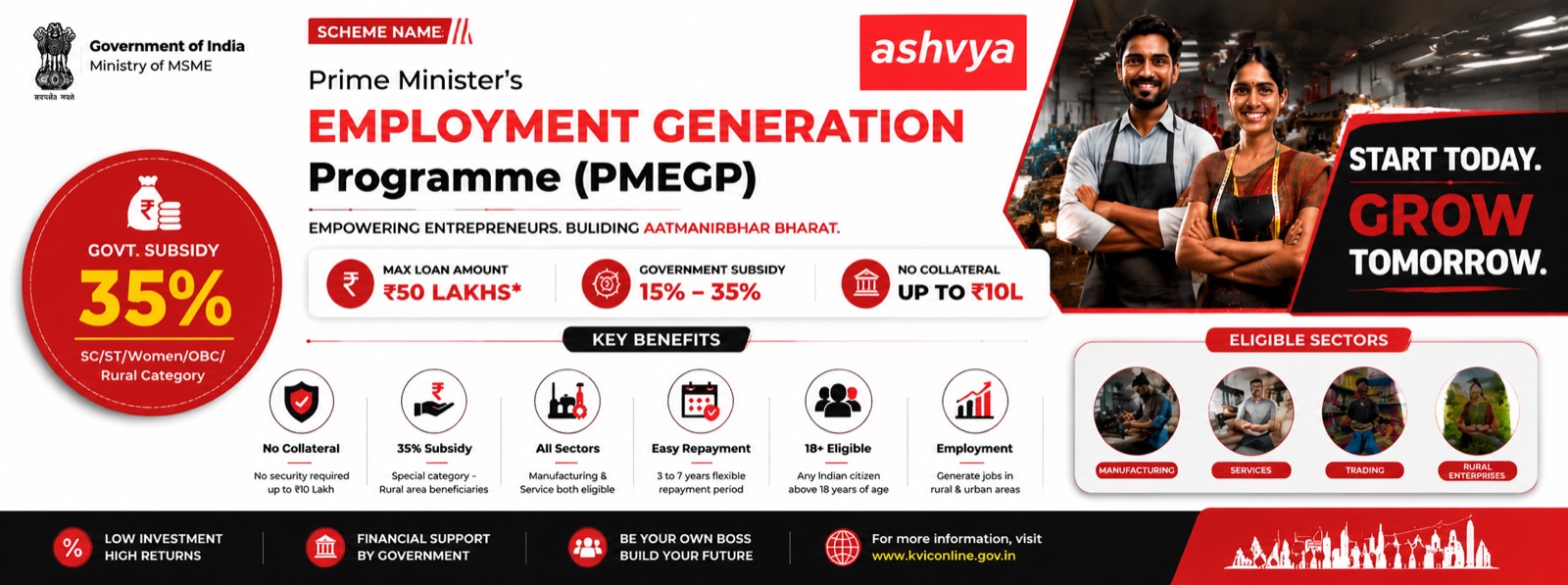

Other collateral-free options

Beyond CGTMSE, Mudra loans, NBFC working-capital lines and government schemes provide unsecured credit.

- Mudra loans up to ₹10 lakh

- NBFC invoice financing

- Stand-Up India for women & SC/ST founders

How to improve your approval odds

Lenders look at cash flow, GST filings and a clean credit history far more than assets.

- Keep GST returns updated

- Maintain a healthy CIBIL score

- Show consistent bank inflows

Tip: Ashvya Services has helped 500+ startups and MSMEs across Vadodara, Surat, Pune and Indore unlock funding and stay compliant. A quick consultation can save you months.

Frequently asked questions

Can a new business get a collateral-free loan?

Yes, through Mudra and certain NBFC products, though limits are lower until you build a track record.

What interest rate should I expect?

Rates vary from ~9% to 18% depending on the lender, scheme and your profile.

How Ashvya Services can help

From eligibility checks to documentation and end-to-end filing, our experts manage the entire Funding & Grants process for you. Talk to an Ashvya expert for a free, no-obligation consultation on collateral-free business loan.

Learn more on the official Startup India portal.